As the year comes to a close, there are multiple questions about the direction of the photography industry. So far, it appears that DSLRs are on the decline, and according to a new report from the Camera & Imaging Products Association (CIPA), there is a mixed view of the market. This raises the question of where DSLR and mirrorless cameras stand today, with the September report largely painting a positive picture. Let’s have a look.

Rise of Compacts

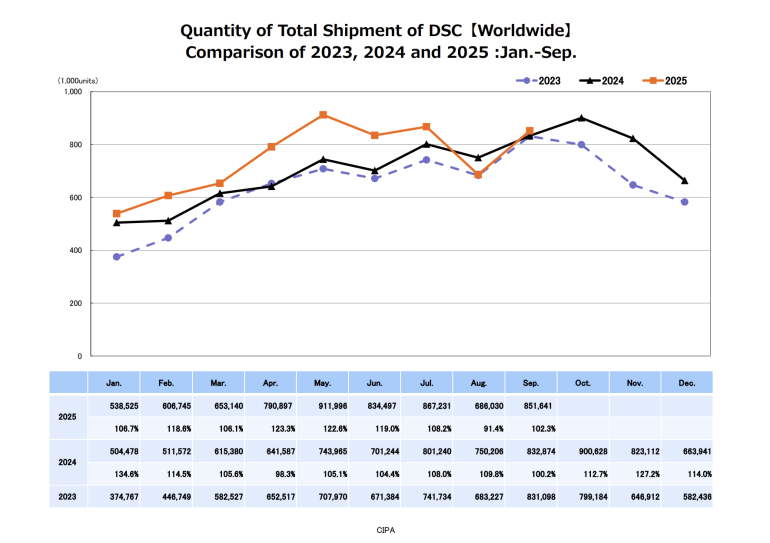

According to the report, the overall camera shipment for September sees a rise in numbers compared to August. This includes cameras across most categories, especially when compared to the September 2024 report. Digital cameras, for instance, reached 880,595 units in production, representing a 22% year-over-year increase. As for the shipments, the number hit 950,112 units, a 19% increase compared to the same month last year. In 2025, this was also the first time camera production reached 6.5 million units, representing a 9% year-on-year increase.

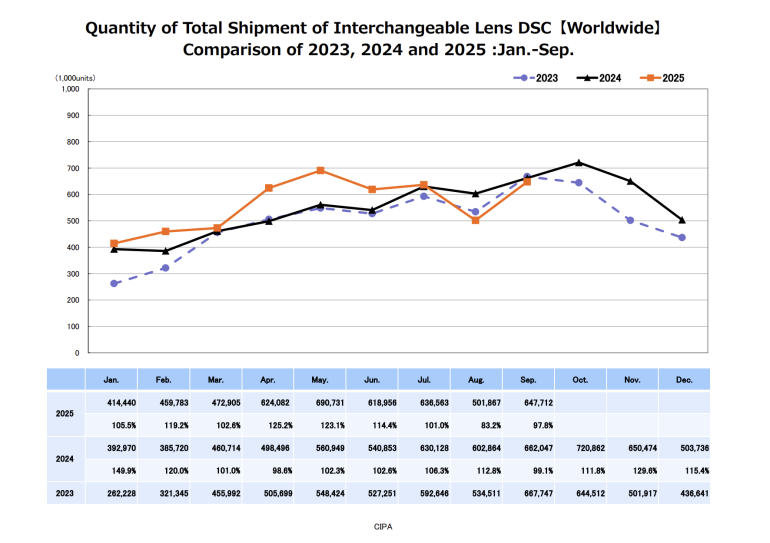

As we pointed out in July 2025, DSLRs are now in decline, and this month’s numbers bear that out. The segment saw a decrease in units (26%) and shipped value (31%) as of September 2025, compared to the same time in 2024. Mirrorless cameras are now wearing the crown, with shipments rising up to 13% in units and 4% in value, which is more than what we saw in the first nine months of 2024. While mirrorless cameras are in demand, the report suggests that the value growth has decreased when compared to last year. This means that sales of mid-range camera bodies are more in demand than those of premium flagships seen earlier. CIPA’s forecast suggests the industry will ship 6.66 million interchangeable cameras across the globe, but the number can go higher by the end of the year.

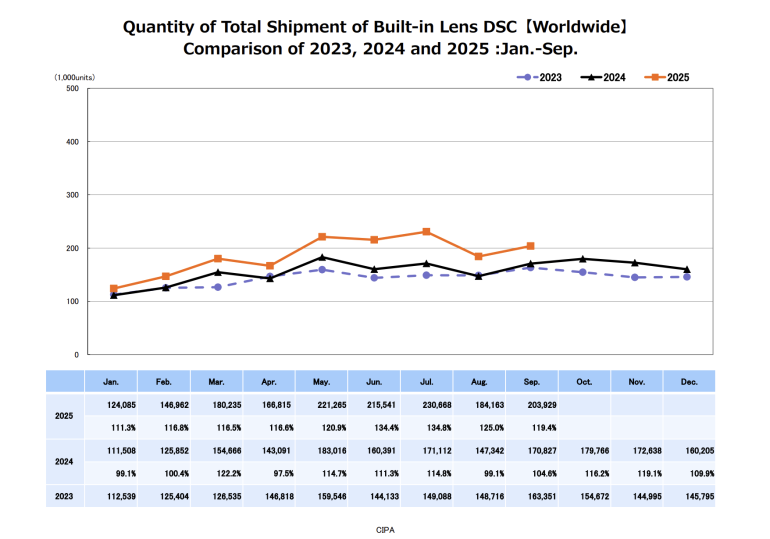

On the other hand, compact cameras also see a continuous resurgence. The shipment value increased by 47%, and the unit shipment rose by 22% year-over-year. This indicates a rise in the average selling price of these devices. One could attribute this to Gen Z and content creators, who opt for models such as Kodak Pixpro, Canon’s IXY series, or Fujifilm‘s X series. Furthermore, the projection for this segment stands at 1.92 million, which further proves that the demand won’t dwindle anytime soon.

Split Trend for Lenses

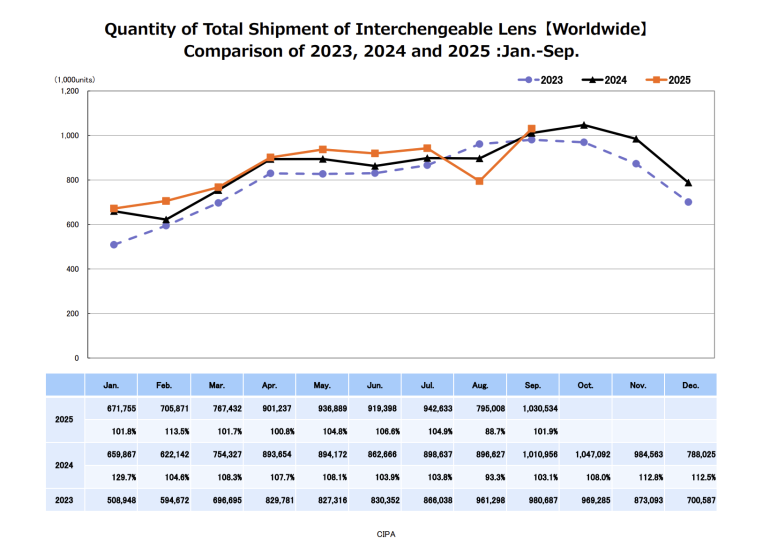

Lenses showcase a different story. Optics for smaller sensors, such as APS-C or MFT sensors, have seen an 18% rise in value and 9% in units. As for full-frame and large-format cameras, the numbers show a decline, with 5% fewer units and 7% fewer units. The slowdown could be a result of people not buying newer systems as often, or that they are happy with the lenses that they already have. The latter also indicates a decrease in the lens-to-body ratio from 1.58 to 1.51 million. In other words, more cameras are being sold today than lenses.

Saturation is one of the reasons why we see stagnant growth for bigger sensor cameras and lenses. Add taxes to the mix, and you will notice regions such as the Americas will continue to face lower shipments. While there is a recovery in numbers compared to the pandemic, there is still some slowness in sales. We have to wait and see what the holiday season brings this year, and how the newer launches impact the larger scale of things.

Get rid of the ads!

Did you enjoy reading this article as much as we enjoyed writing it? There's a way to support us and our reporting, getting ad-free navigation and more as a bonus. Subscribe to us for less than a coffee per month —just $3.99— or take advantage of our yearly subscription with a hefty discount for only $25.- An ad-free experience

- A free mystery box for Lightroom or Capture One

- All the books in our store

- 20% discount on Capture One

- 30% discount on Imalume Photo Theft Protection

- 20% off Herbs and Kettle Tea Company.